2025 Inbound Logistics Perspectives: 3PL Market Research Report

Amid policy shifts and uncertainty, geopolitical volatility, and fast-rising new technology solutions, third-party logistics (3PL) providers are adopting and evolving to serve the changing needs of their clients. The 2025 Inbound Logistics 3PL Perspectives report highlights how recent adjustments are shaping 3PL services and operations, while also revealing shifts in the diverse shipper landscape they support.

This year, which marks the 20th year of the report, we see some formerly trending topics such as sustainability and blockchain losing traction, while others—artificial intelligence, of course—gaining steam. It also shows that even as 3PLs point to the increased difficulty of finding and retaining clients in the current climate, they are enjoying profitability at a higher rate than one year ago.

After you read the report, peruse our list of the 2025 Top 100 3PLs (page 74) to learn more about the leaders in the field and the vital role that they play for shippers, helping to manage supply chains that grow more complex—and critical—with every passing year.

ABOUT THE 3PL RESPONDENTS

ASSET-BASED OR NON-ASSET BASED:

Both: 57%

Non-asset: 36%

Asset-based: 7%

GEOGRAPHIC COVERAGE:

North America: 41%

Global: 35%

U.S. Only: 24%

This year’s participating 3PL respondents report a total of more than $196 billion in gross sales in 2024 (though not all participants share sales numbers). That number is up $2 billion from last year, a relatively modest increase compared to the $21-billion uptick that was reflected in the 2023 survey. Nevertheless the data suggests that despite global friction, total revenues have increased from 2023.

Of this year’s respondents, 57% of 3PLs offer both asset-based and non-asset based services, 36% define themselves as non-asset-based, and a mere 7% are asset-based only. Meanwhile, 41% focus their coverage on North America, 35% offer global coverage, and 24% service the U.S. only.

MARKETS SERVED:

Transportation: 90%

Manufacturing: 83%

Retail: 83%

Ecommerce: 68%

Wholesale: 67%

Services/Government: 52%

Transportation remains the leading market served, with 90% of 3PLs reporting it as one of their primary areas of operation. Other top verticals served include manufacturing (83%, down four percentage points from last year) and retail (83%, down a sharp eight percentage points from 2023). Ecommerce holds steady in the fourth spot, though the 68% of providers serving it marks a six-point decline from two years ago.

Notably, the survey shows a stark drop in providers serving the wholesale market, declining from 83% in 2023 to 76% last year, and all the way to 67% in this year’s report. Meanwhile, the services/government sector remains the most underserved of the categories captured on the survey, with just 52% of providers including it in their clientele—down five points from last year.

Top Challenges Shippers Face

Shippers are contending with an array of challenges, but this year’s survey respondents seem to be less concerned than they were last year. For instance, cutting transport costs continues to be the most-cited challenge, but the percentage of shippers who view it that way dropped from 41% to 32% in one year. Other top shipper challenges also show marked declines in the past year, including business process improvement (22%, down 11 percentage points), improving customer service (18%, down 10 points) and supply chain visibility (16%, down nine points).

Shippers are contending with an array of challenges, but this year’s survey respondents seem to be less concerned than they were last year. For instance, cutting transport costs continues to be the most-cited challenge, but the percentage of shippers who view it that way dropped from 41% to 32% in one year. Other top shipper challenges also show marked declines in the past year, including business process improvement (22%, down 11 percentage points), improving customer service (18%, down 10 points) and supply chain visibility (16%, down nine points).

Also mentioned at a lower rate than last year are: managing inventory (15%, down four points); reducing labor costs (14%, down five points); expanding to new markets via selling (11%, down one point); finding, training, and retaining qualified labor (11%, down five points,); and technology strategy and implementation (10%, down three points).

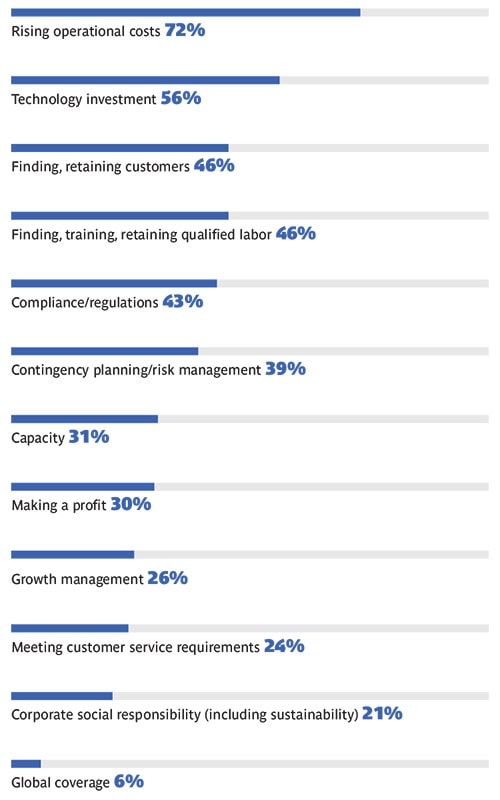

Top Challenges 3PLs Face

When it comes to challenges facing 3PLs, the top of this year’s survey looks like the top of last year’s survey: rising operational costs remain well-entrenched at No. 1, receiving a vote from 72% of respondents—down just one point from 2024. However, in general, the survey shows major shifts in 3PL challenges.

When it comes to challenges facing 3PLs, the top of this year’s survey looks like the top of last year’s survey: rising operational costs remain well-entrenched at No. 1, receiving a vote from 72% of respondents—down just one point from 2024. However, in general, the survey shows major shifts in 3PL challenges.

For instance, technology investment lands well back in the No. 2 slot at 56%, reflecting a decline of 10 percentage points in two years as more 3PLs become comfortable in that area. Meanwhile, heading in the opposite direction, the third-biggest challenge among respondents this year is finding and retaining customers—surging 13 points to 46% in two years, suggesting the competition for clients has grown more intense.

Other 3PL challenges logging major declines include finding, training, and retaining qualified labor (46%, down 13 points since 2023—a hopeful sign for the enduring staffing issues that have afflicted many in the industry); capacity (31%, down 15 points); and corporate responsibility, including sustainability (21%, down a striking 17 points as policy shifts undermine the previous emphasis in that area). Not everything has gotten easier, though. Compliance/regulations (43%, up 11 points), contingency planning/risk management (39%, up 12 points), and making a profit (30%, up 14 points) have all grown harder in the past two years, according to 3PL respondents.

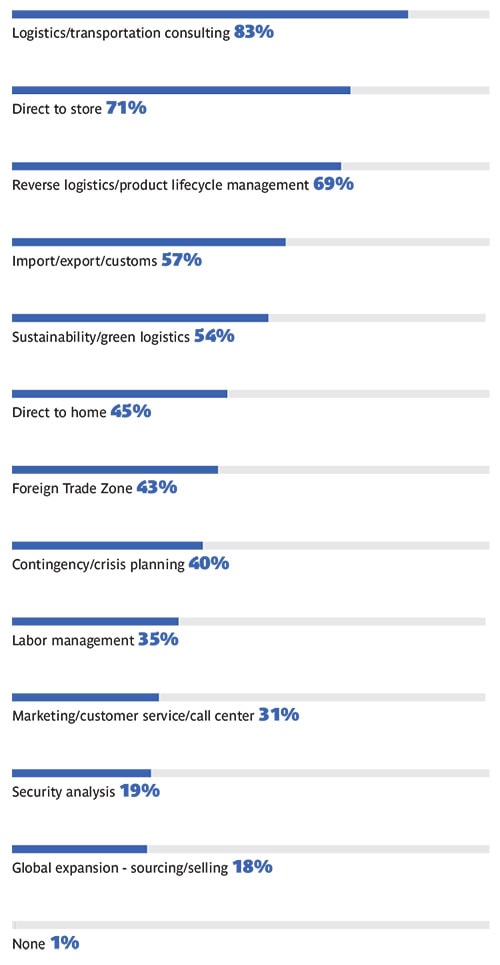

Special Services 3PLs Offer

The top five special services 3PLs offer this year are logistics/transportation consulting (83%), direct to store (71%), reverse logistics/product lifecycle management (69%), import/export/customs (57%), and sustainability/green logistics (54%). Those were also the five most-popular special services in last year’s survey, but sustainability/green logistics dropped 12 points from one year ago and fell from third to fifth in the rankings—another sign of a shift away from that once-ascendant priority. Among the big movers lower down the rankings, foreign trade zone jumped 14 points to 43% in the past two years, highlighting a growing area of opportunity for providers.

The top five special services 3PLs offer this year are logistics/transportation consulting (83%), direct to store (71%), reverse logistics/product lifecycle management (69%), import/export/customs (57%), and sustainability/green logistics (54%). Those were also the five most-popular special services in last year’s survey, but sustainability/green logistics dropped 12 points from one year ago and fell from third to fifth in the rankings—another sign of a shift away from that once-ascendant priority. Among the big movers lower down the rankings, foreign trade zone jumped 14 points to 43% in the past two years, highlighting a growing area of opportunity for providers.

Shippers, What is the Top Reason for a Failed 3PL Partnership?

Shippers, Is Price or Service More Important?

Two years ago, a whopping 60% of shipper respondents listed poor customer service as the top reason for a failed 3PL partnership, but that number declined to 36% last year and dropped another two points to 34% this year. However, it still is shippers’ No. 1 reason for a failed partnership, topping failed expectations (28%) and cost (22%). Shippers overwhelmingly consider service to be more important than price by a count of 72% to 28%.

Two years ago, a whopping 60% of shipper respondents listed poor customer service as the top reason for a failed 3PL partnership, but that number declined to 36% last year and dropped another two points to 34% this year. However, it still is shippers’ No. 1 reason for a failed partnership, topping failed expectations (28%) and cost (22%). Shippers overwhelmingly consider service to be more important than price by a count of 72% to 28%.

Strategies Shippers and 3PLs Use to Manage Challenges

When navigating challenges, shippers and 3PLs use a host of approaches. This year, 59% of respondents point to nearshoring or reshoring as a strategy they favor, while close behind, 58% say they use supply chain design. Other common strategies include DC network optimization and realignment (54%), lean best practices (54%), and strategic sourcing strategies (50%). Supply chain decentralization posted the largest jump in the category, rising eight percentage points to 26% in one year.

When navigating challenges, shippers and 3PLs use a host of approaches. This year, 59% of respondents point to nearshoring or reshoring as a strategy they favor, while close behind, 58% say they use supply chain design. Other common strategies include DC network optimization and realignment (54%), lean best practices (54%), and strategic sourcing strategies (50%). Supply chain decentralization posted the largest jump in the category, rising eight percentage points to 26% in one year.

Should Shippers Partner with One or More 3PLs?

On the question of whether shippers should partner with more than one 3PL, the replies are nearly identical to last year’s survey, with 40% saying it depends, 33% saying they should stick to one 3PL, and 27% saying more than one is preferrable.

On the question of whether shippers should partner with more than one 3PL, the replies are nearly identical to last year’s survey, with 40% saying it depends, 33% saying they should stick to one 3PL, and 27% saying more than one is preferrable.

Those who advocate for just one 3PL point to the value of consistency of processes, while those who see the benefits of working with multiple 3PLs note the advantages of a diversification of providers and the possible need for different areas of specialization.

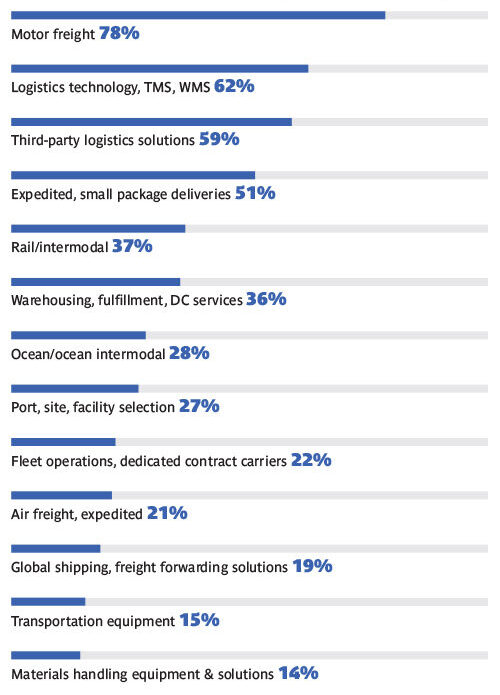

Services Shippers Buy

The services shippers purchase have shifted significantly over the past two years, with many seeing dramatic declines in the 2025 survey. Motor freight, at 78%, ranks highest among respondents. Logistics technology, TMS, and WMS, ranks second at 62%, which reflects a 10-point drop from last year.

The services shippers purchase have shifted significantly over the past two years, with many seeing dramatic declines in the 2025 survey. Motor freight, at 78%, ranks highest among respondents. Logistics technology, TMS, and WMS, ranks second at 62%, which reflects a 10-point drop from last year.

Other critical services, cited by more than half of respondents, include third-party logistics solutions (59%, down 10 points from last year) and expedited, small package deliveries (51%, down 23 points). Among services seeing the steepest declines are warehousing, fulfillment DC services (down 28 points to 36%); ocean/ocean intermodal (down 16 points to 28%); air freight, expedited (down 33 points to 21%); global shipping, freight forwarding solutions (down 21 points to 19%); and materials handling equipment & solutions (down 21 points to 14%). No area saw a similarly notable increase in the report.

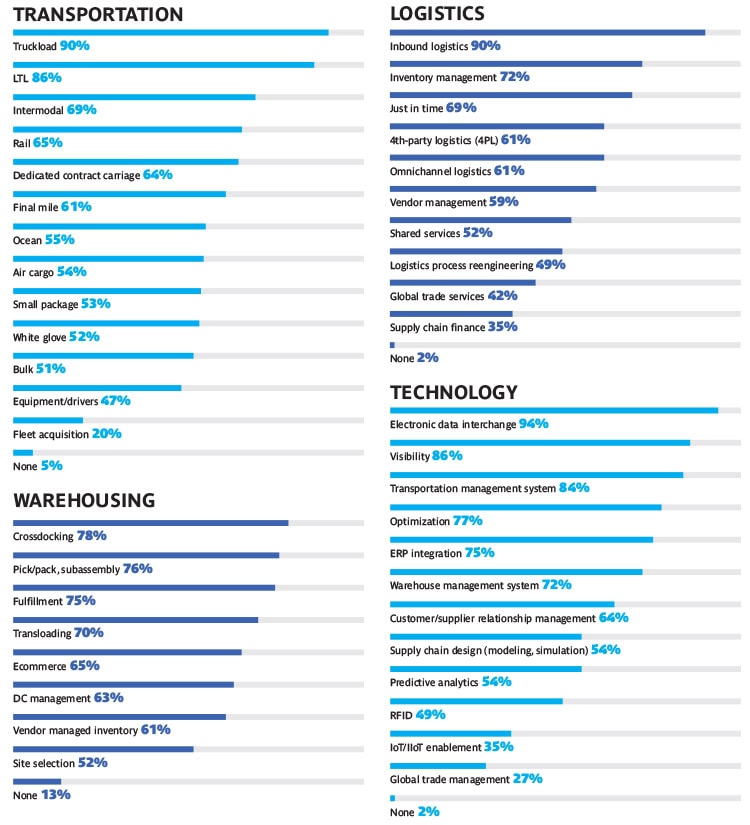

3PL Services & Capabilities

The transportation services and capabilities 3PLs provide have remained steady over the past three years. Truckload (90%) and LTL (86%) are the clear No. 1 and No. 2, with intermodal (69%), rail (65%), and dedicated contract carriage (64%) rounding out the top five. The most common logistics services and capabilities are inbound logistics (90%), inventory management (72%), just in time (69%), 4th-party logistics (61%), and omnichannel logistics (61%).

Electronic data interchange (94%) repeats again this year as No. 1 among technology services and capabilities offered by 3PLs, followed by visibility (86%), transportation management system (84%), optimization (77%), and ERP integration (75%).

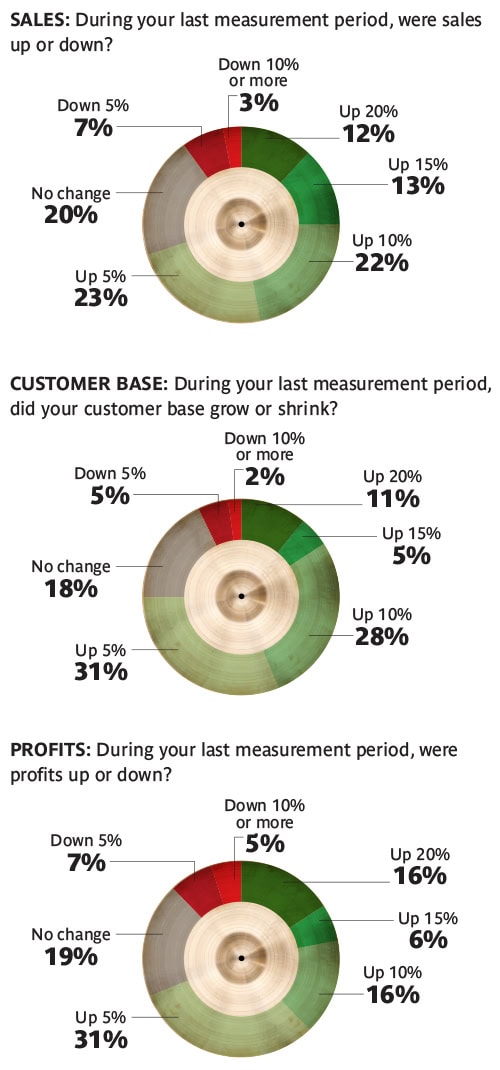

3PL respondents report healthy sales during their most recent measurement period. Twelve percent cite sales growth of 20% or more, while 13% say they are up approximately 15%. Another 45% report growth of 5% or 10%. The most significant shifts from last year appear at the lower end of the sales spectrum. Only 3% of respondents report a sales decline of 10% or more—down from 13% in 2024. But that doesn’t mean everyone experienced strong growth: 20% report flat sales, a six-point increase over last year. Among those who saw no growth or a loss, some point to a soft freight demand environment as keeping sales muted.

3PL respondents report healthy sales during their most recent measurement period. Twelve percent cite sales growth of 20% or more, while 13% say they are up approximately 15%. Another 45% report growth of 5% or 10%. The most significant shifts from last year appear at the lower end of the sales spectrum. Only 3% of respondents report a sales decline of 10% or more—down from 13% in 2024. But that doesn’t mean everyone experienced strong growth: 20% report flat sales, a six-point increase over last year. Among those who saw no growth or a loss, some point to a soft freight demand environment as keeping sales muted.

Meanwhile, growth in customer base this year is very similar to 2024: 11% of respondents say their customer base increased 20% or more—matching last year—and 5% report growth at the 15% threshold, down 2 points from 2024. Of interest, only 2% indicate a drop of 10% or more to their customer base, the smallest number in the past three surveys.

Profits are decidedly up among respondents, with 69% reporting profit of some kind in the most recent measurement period, a jump of nine points from one year ago. That includes 16% seeing growth of 20% or more, a full seven points higher than 2024.

Only 5% of respondents saw profits drop by 10% or more—down from 13% last year. While inflation pressured margins, many credit gains to improved efficiency through technology and automation.

Most Impactful Technologies

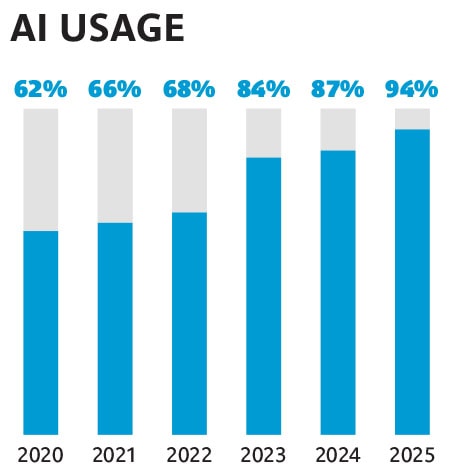

Artificial intelligence’s dramatic impact on the 3PL sector is undeniable (see chart below for the increase in usage since 2020). Respondents show AI as the clear-cut winner when asked about the most impactful technologies in the field, garnering 94% of replies. This marks an increase of 10 percentage points in the past two years.

Artificial intelligence’s dramatic impact on the 3PL sector is undeniable (see chart below for the increase in usage since 2020). Respondents show AI as the clear-cut winner when asked about the most impactful technologies in the field, garnering 94% of replies. This marks an increase of 10 percentage points in the past two years.

Ranking in a distant second place (46%)among impactful technologies is driverless vehicles. Other technologies on the impactful list have faded in prominence since last year, according to respondents, especially Internet of Things (24%, down 16 points in two years), blockchain (18%, down 10 points), and wearable technology (13%, down 10 points).